Sustainability, at its heart, is avoiding borrowing from the future to pay for the present. What can companies and investors do now to put them in the best position later?

Sustainability, at its heart, is avoiding borrowing from the future to pay for the present. What can companies and investors do now to put them in the best position later?

Companies often suggest that sustainability lies at the core of their business strategy and directly impacts their long-term profitability. At the individual company level, it pays more to operate sustainably – we know that allocating capital to R&D, investing in employees, and aligning with key stakeholders and long-term shareholders sets companies up for far greater value creation and ROI than grasping for short-term gains.

Ideally, investors are rewarded for their patience when these sustainability initiatives pay off. But in the meantime, corporate leaders feel that their sustainability initiatives are being thwarted from almost every angle. Activists are riding an anti-ESG wave prioritizing short-term profitability, and many investors remain skeptical of corporate sustainability investments due to unclear payoffs, misaligned time horizons, and confusing messaging. Fearing for their future, many companies have changed tack from trumpeting sustainability efforts to “green hushing.”

What exactly is it that companies see but investors don’t? Externalities – defined by Engine No.1’s Chris James and Wharton’s Vit Henisz as “uncompensated consequences of production or consumption that impact third parties and are not reflected in market prices” – are at the center of the debate. Negative externalities are elements of the business or biproducts of production that may be afterthoughts and unaccounted for today, but could incur a real cost down the line. For example, chlorofluorocarbons (CFCs) in the 1990s were not considered an issue 30 years ago, but are a consequential cost today; whereas positive externalities, like COVID vaccines, not only provide a financial boost to Pfizer and Moderna, but also promote herd immunity, preventing further spread of the disease.

Some externalities may be uncompensated forever. Recognizing which externalities will go from uncompensated to compensated – or later internalized and either paid for or rewarded – is critical to creating long-term value. Companies are constantly evaluating externalities and the likelihood that they will be internalized, and the good ones are factoring them into their long-term strategies today. Doing so goes a long way to reduce future costs, boost returns, and brace the company to withstand volatility.

But here’s the rub – companies and investors don’t always agree on what to prioritize. Plans laid out with the best intentions to buffer the company’s long-term survival against whatever may come might clash with investors’ short-term goals or portfolio objectives. The best ideas on paper – and the value they could have created – can’t materialize if investors cut and run too early. And even when investors do share a company’s vision, we can’t blame them for being skeptical that the company will benefit over time. So where does this leave our companies and investors trying to invest for an uncertain future? How can the real long-term companies with solid strategies communicate them to the real long-term investors?

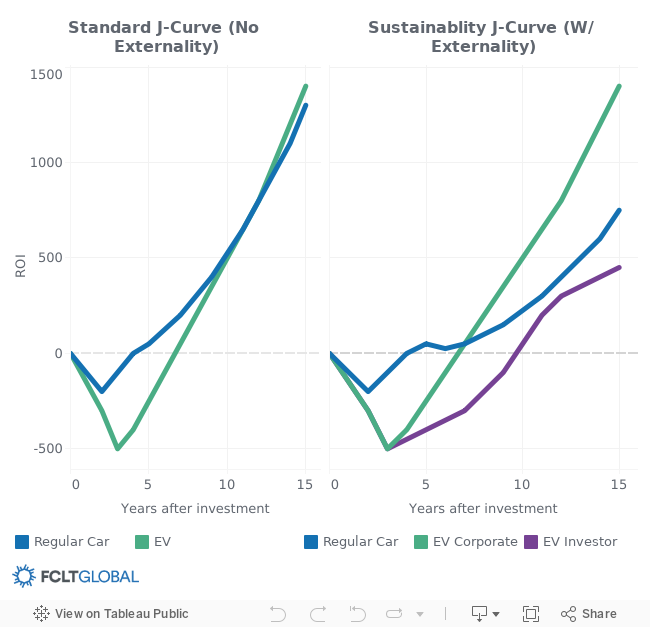

Communicating the plan might be more effective if investors can literally see the point. Consider an auto company choosing between investing in the development of a regular car versus an electric vehicle (EV). As seen on the left panel of Figure 1, initiatives are straightforward to evaluate with standard j-curves. Choose the ones that make the most money (invest in a regular car) and avoid the ones that lose money (EV). Fair enough, but sustainable J-curves are trickier and the initiatives behind them take more time to implement – which will surely filter out the short-term-oriented investors.

Figure 1: The Standard and Sustainable J-Curves

In the sustainable j-curves frameworks, companies decide to ‘internalize the externalities’ – or factor the potential future costs into decision-making and recognize the risk.

The right side of Figure 1 adds the negative externality of a carbon price into the equation, starting in year 6. In this framework, EV cars look like the better investment from the company’s point of view (seen here as a green line). However, if an investor disagrees with the company’s assessment of the timing and size of a future carbon price (purple line), or simply has a shorter horizon, it may encourage the company to choose the regular auto option.

Figure 2: The Sustainable J-curve Framework

Thus, when companies communicate their sustainability strategy, instead of empty talk stressing how important sustainability is to their business, illustrating the assumptions in a practical way that investors recognize will drive home the point. A matrix-like framework similar to that of Figure 2 highlights that the goal of their sustainability initiatives is to have investments moving from bottom-left to top-right, given enough vision, time and patience.

In our car example, perhaps the EV is not yet compelling with current pricing (i.e., no carbon tax or EV subsidy) but could be very compelling in a potential future regime.

As such, companies and investors that get the shape and profile of the sustainable j-curve right can be rewarded spectacularly in the long run. BYD and Iberdrola are examples of sustainability J-curve success stories (Figure 3):

Figure 3: Companies realizing financial value from long-term sustainability strategies

| Company | Externality | Challenge | Solution |

|---|---|---|---|

| BYD | Traditional cars emit a lot of GHGs and may be subject to carbon taxes in the future; gas has and will become more expensive | Limited battery range and EV infrastructure; EV price uncompetitive vs. gasoline cars | Reinvested initial cellphone battery profits into adjacent EV R&D, vertical integration (vehicles, motors, controllers) with existing manufacturing plants; built EV cars with large range at affordable prices |

| Iberdrola | 1997 Kyoto protocol set ambitious emissions reduction targets, causing uncertainty for high emitting sectors | Hard to adapt to impending stricter regulations while maintaining profitability and growth | Recommitted to core competency in renewables, scaling up operations in wind, solar and storage capacity; Today, continuing to anticipate new sources of electricity demand |

Using the sustainability J-curve as a tool for visualizing strategies that may not pay off today, but will likely pay off over time, will promote better company-investor dialogue, which in turn will help more ideas, innovations, and long-term rewards see the light of day.

The next phase of this research is to explore more examples of success stories and discover what they have in common. What did they do well that can be applied broadly? What obstacles did they face and how did they overcome them? We would also like to hear examples of initiatives that seemed destined for success and failed. What went wrong? If you have a story to share, we’d love to hear from you – please reach out to [email protected].

Risk and Resilience | Report

11 April 2022 - An Adaptable, Top-Down Approach to Addressing Climate Change in Investment Portfolios

Metrics | Report

26 April 2023 - As companies around the world begin to make the shift to more sustainable practices, private markets have the potential to drive substantial investment in the "grey-to-green" transition by investing in high-carbon-emitting sectors with the goal of reducing their emissions over time. However, concerns around returns, metrics, and reputational impacts are limiting greater participation.

Risk and Resilience | Report

21 December 2018 - Boards and executives of long-term funds, such as pension plans, sovereign wealth funds, and endowments, have a challenging problem. They need to manage those portfolios to meet their long-term purpose, which may be decades or more into the future. Yet no fund has the luxury of looking only to that long-term time horizon. Each must also meet expectations in the near term in order to continue in its role and with its investment strategy.