In a decade-long low interest rate environment, riskier asset classes have seen accelerated asset gathering as savers chase yield.

In a decade-long low interest rate environment, riskier asset classes have seen accelerated asset gathering as savers chase yield.

By Allen He

Interest rates were in an all-time low over the ten-year span from 2009-2018, particularly in the world’s largest economies. The United States, the United Kingdom, France, Germany, Italy, Japan, Canada all had zero, near-zero, or even negative interest rates between 2009-18, far lower than historical averages. Data from FCLTCompass shows that this has led to many investors taking on more risk to chase yield and return as historically “safe” assets, like treasury bills, money-market funds, and investment-grade corporate bonds on average no longer yield as much as in the decades before the recession.

While riskier asset classes have seen a rise in popularity and capital allocation as of late, trends can be seen through the decision-making of various savers groups.

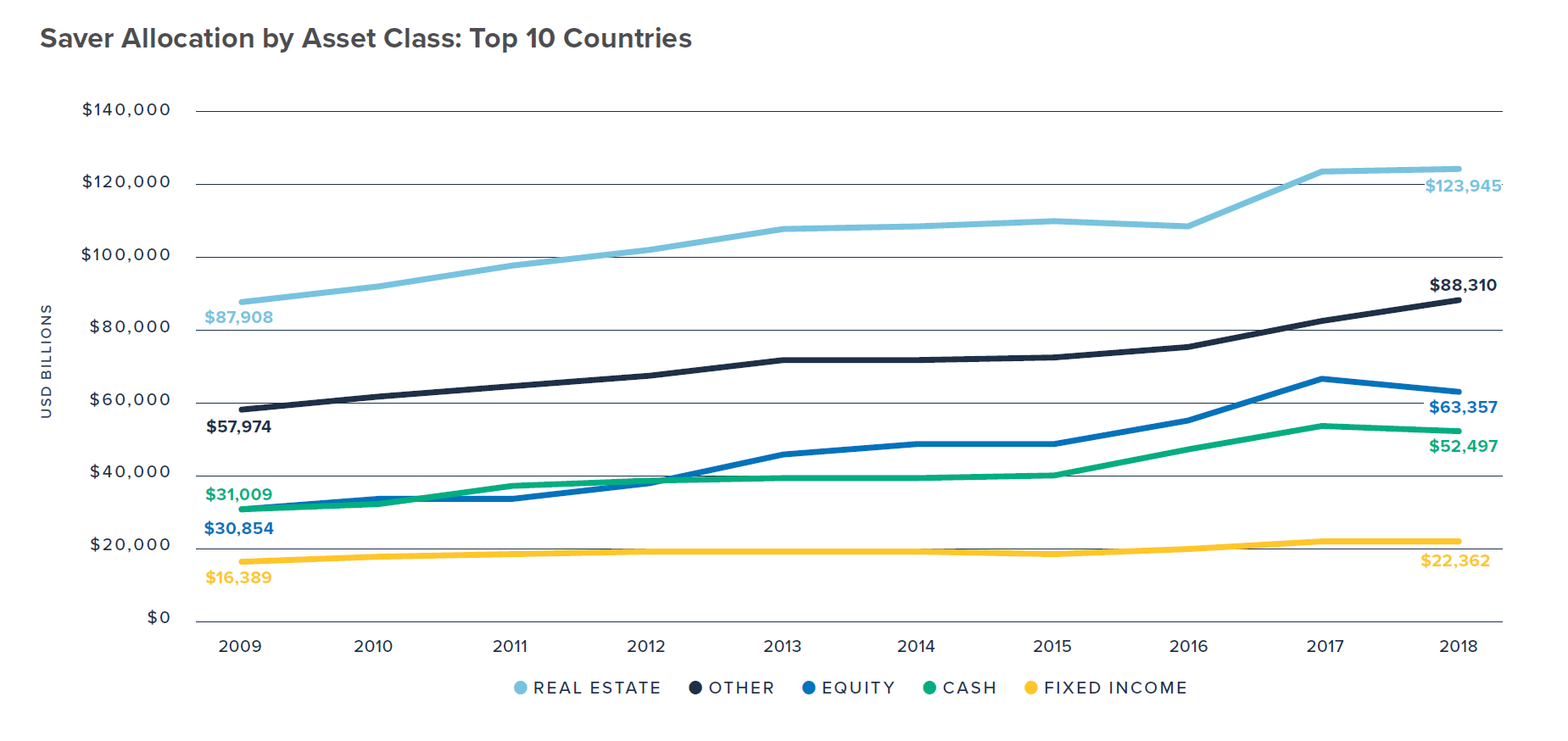

Fixed income continues to grow, but that growth has stagnated considerably compared to rates of other assets – $16T allocated in 2009 compared to $22T in 2018. Fixed income, while traditionally less risky than other asset classes like equity and alternatives, has lower return, which can be seen as a driving force behind the gradual decline. At the same time, savers’ investments in equities have more than doubled in that same timeframe – $63T in 2018 up from $31T ten years prior.

Pensions in particular have shifted allocation more towards equity (and other emerging asset classes) and away from fixed income, due to the lower yields compromising their need to meet future obligations. This new direction adds diversification to the pension portfolios (and higher potential returns, but will produce a different risk profile and wider range of potential outcomes.

Likewise, other saver groups with longer-term intended horizons – sovereign wealth funds or endowments, for example – have moved capital towards alternatives like private equity (up from $52B in 2009 to $127B in 2018) or hedge funds (from $71B to $114B). With longer investment horizons and lower immediate drawdowns than pensions, endowments and sovereign wealth funds may continue to shift towards these high-risk, high-reward alternatives which often feature substantial lock-up periods, limiting liquidity in the short-term.

Going forward, with interest rates expected to remain low both in major economies and developing markets, a transition away from fixed income may be the “new normal” For savers and investors, this may mean that risk profiles will look quite different than what they’ve grown accustomed to. Moving from fixed income to equities shortens investment time horizons, counterbalanced by moving more money into long-range alternative asset classes like infrastructure, private debt, and real estate. The impact these trends have on the larger investment horizons for savers worldwide remains to be seen.

Trends toward longer equities investment horizons have been promising, and FCLTGlobal will continue to monitor these trends in the next refresh of the FCLTCompass dashboard, due out in late 2021. To learn more about the project and see more data about global long-term investment trends, click here.

18 December 2024 - FCLT Compass is a dashboard measuring the investment horizons of the global investment value chain, how households are saving and allocating their money, and how long they can live off those savings. Calculating these metrics provides a holistic understanding of the long- or short-term orientation of global capital markets and how that orientation impacts the financial futures of millions of people worldwide.